First paycheck arrives… and voila!

Your whole outlook on life just changes.

Not because it’s big.Because it’s real.

You open your banking app once.Then again.

Just to make sure you’re not dreaming.

Then one question just subtly starts coming up:

"Alright... what's next?"

And that's when it all begins to diverge.

Some people:

- Spend all of it.

- Save what’s left over.

- Plan for everything else later.

And that later is precisely where money behaviour gets quietly programmed.

Not at once.

Not deliberately.

But simply through repetition.

So before your salary is transformed into

Subscriptions,

Swiggy deliveries,

And small impulse buys that are far from being actually small…

Below is a 7-step checklist.

That can determine

Your financial future without turning you into an economic student.

1. Let your lifestyle arrive slower than your salary

The first salary arrives with a silent desire:“I am finally able to buy this/that”

And yes, enjoying it matters.

But there’s a strong trend that most financially stable people adhere to:

They hold back on their lifestyle expansion a bit.

Not completely stopping it.

Just slowing it.

Because when your spending increases at the same rate as your income,

There is nothing left behind.

But when your income starts growing a little faster than your lifestyle?

That difference is your financial base.

It’s not much right now.

It’s all that matters later.

2. Build a “life buffer” before anything else

Before investing, before planning, before goals …

There is one unspoken priority: Stability cushion

Consider this your financial pause button, an emergency fund.

It helps you deal with those times when things don’t go according to plan:

- Unplanned trip

- Medical crisis

- Emergencies

- Breaks

And if that occurs, then this buffer ensures that all other things are stable.

- No disruption to plans

- No rearrangement of decisions

- No financial stress mode

This is not preparation against any potential issues.

This is preparation for reality amid all other activities.

And such stability provides a definite advantage in the long run.

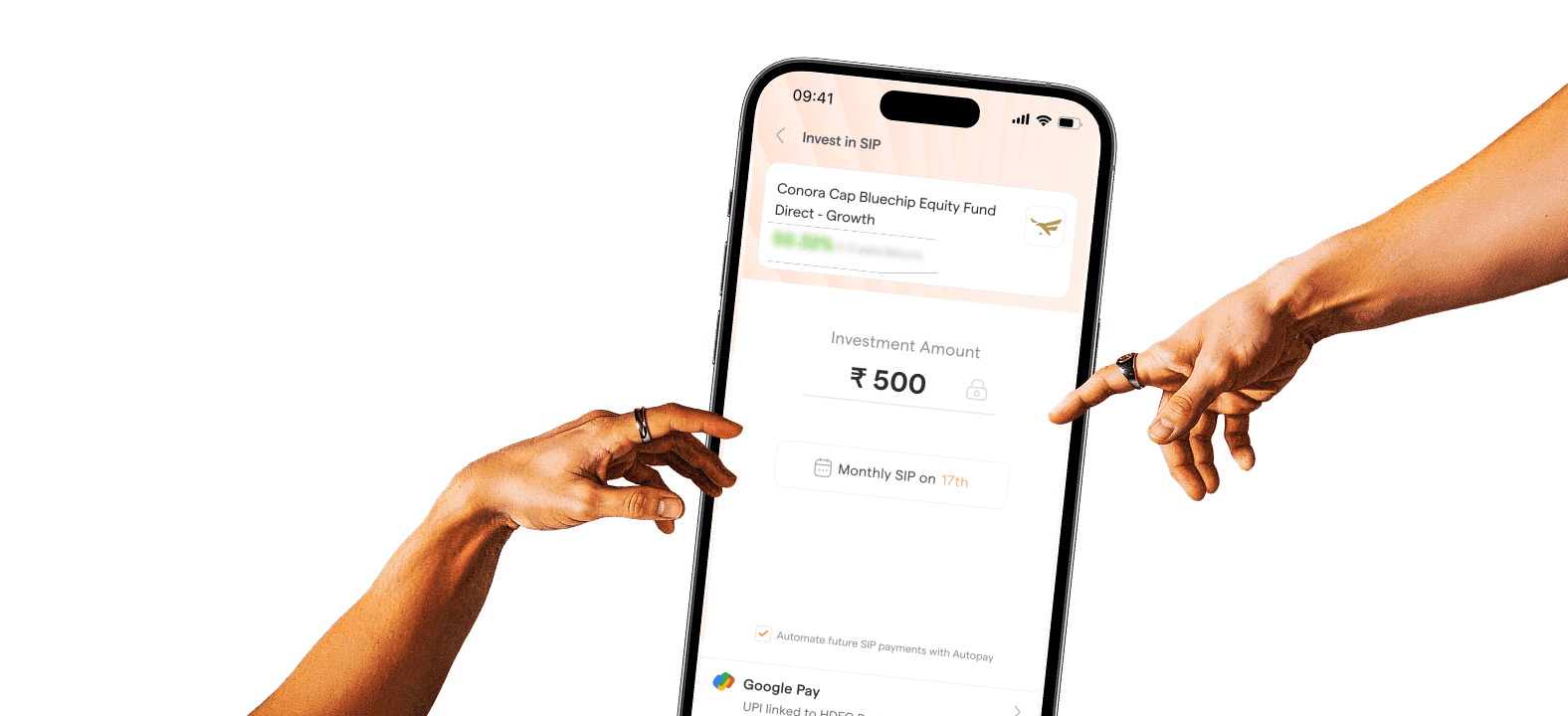

3. Start investing so small it feels almost too easy

How to invest your first salary?

Here is where most people tend to over analyse things.

"I will begin once I earn more."

"I will begin once I know more."

"I will begin next month."

But investments never favour good timing.

They always favour early beginnings.

Even a small SIP creates something bigger than returns.

It creates an identity.

You move from saying "I should be investing" to "I am investing".

That is all it takes.

Why?

Because wealth isn’t created by a single big decision.

It’s created by several repeated decisions running silently in the background.

4. Learn where your salary actually goes

It always shocks most people.

First salary goes quickly.

Not because of one huge expense.

In small repetitive spending on:

- Subscriptions

- Impulse buys

- Spending out of convenience

- Small internet purchases

That's why expense tracking is extremely important.

Not to limit you.

But to get to know your spending habits.

Since financial awareness is what transforms earnings into real wealth creation.

If you know how your money flows,

You will likely make better decisions subconsciously.

5. Start health coverage early while everything is simple

This is something most young earners tend to delay.

Since health insurance always appears as a ‘later’ choice.

Until you encounter one expense that makes it an immediate matter.

But,

It’s cheaper to have your health insurance at a younger age.

Also, there are numerous advantages when you purchase early, too.

Even if you are insured by your employer,

Knowing your health coverage early enough financially is a wise decision.

Building wealth goes smoothly only if no unexpected costs disturb you.

6. Avoid building your financial knowledge through random internet noise

Financial tips are provided every single minute on the internet.

- Best stocKS

- Faster way to become rich

- The best SIP

- Retire at 30

The issue is:

All of them may not suit your

Income levels,

Your financial goals,

And the comfort level with regard to risks.

That is why your early earning years should pay less attention to seeking out “the perfect investments”…

And more to financial basics, like:

- Budgeting

- Emergency savings

- Compound interest

- Taxation

- SIP

These basics continue to apply regardless of income or economic situation.

And in the long run,

They matter much more than any financial trend news.

That is precisely why all the best first salary financial tips in India invariably

Come down to just one thing – understand first, react later.

7. Use your first salary to build systems, not just memories

Yes, celebrate that first pay.

Buy something significant.

Treat your family to something.

Build memories around it.

But along with celebrating,

Also set up systems like:

- Automating savings

- SIPs

- Expense tracking

- Financial goals

Because systems avoid decision fatigue.

Those who set up such automation early in life

Tend to keep going for years on end without trying harder.

This is when managing money gets easier.

Final thought: your first salary isn’t the start of income, it’s the start of a pattern

This is the true transformation.

The amount doesn't matter

As much as the habits around the amount.

Because what the initial pay silently plants is:

financial freedom.

And the way you conduct yourself in this stage can reverberate for decades due to:

- Behaviour in spending

- Consistency in investing

- Saving habits

- Lifestyle choices

So yes, celebrate it to the fullest.

But make sure

At least a small portion works silently to secure your future, too.

Since the most intelligent decision regarding your first salary

Would never be an exciting one.

But creating a system which works

Even after you no longer get excited by the first salary notification.