The 50 30 20 rule, it sounds great in theory.

An even split. Basic math. Popular finance rule.

- 50% needs.

- 30% wants.

- 20% savings.

Done but life doesn't operate on percentages. Rent is expensive.

Expenses do not fall into convenient buckets and life itself has its own flow.

And then suddenly, We’re left with a very real question:

“Can the 50-30-20 budgeting rule really work in real life?”

Let’s look at things from the perspective of how finances behave outside of spreadsheets.

First, what this rule is trying to fix

Most people don’t have an income issue. Their problem lies in budgeting it. Money flows in. Money flows out.

But in between… they lose track of where it all went.

That’s where the 50 30 20 rule comes in handy. It allocates your money into three main areas:

50% → Life basics (Needs)

This is your non-negotiable expenditure area.

- Rent/Utilities

- Grocery

- Electricity/Broadband/Phone Bills

- Transport

- EMI, if any

This is the one that keeps life going in a normal way.

Once this starts ballooning,

Everything else will be automatically squeezed.

This is the reason why this bucket ends up deciding your financial stability silently.

30% → Life enjoyment (Wants)

This is where life starts to become bearable.

- Food delivery

- Dining out

- Shopping

- Travel

- Entertainment

Nothing here is vital for survival.

But everything in this category brings comfort and pleasure.

Without this category,

It’s impossible to budget realistically.

Without it being controlled,

It causes savings to evaporate.

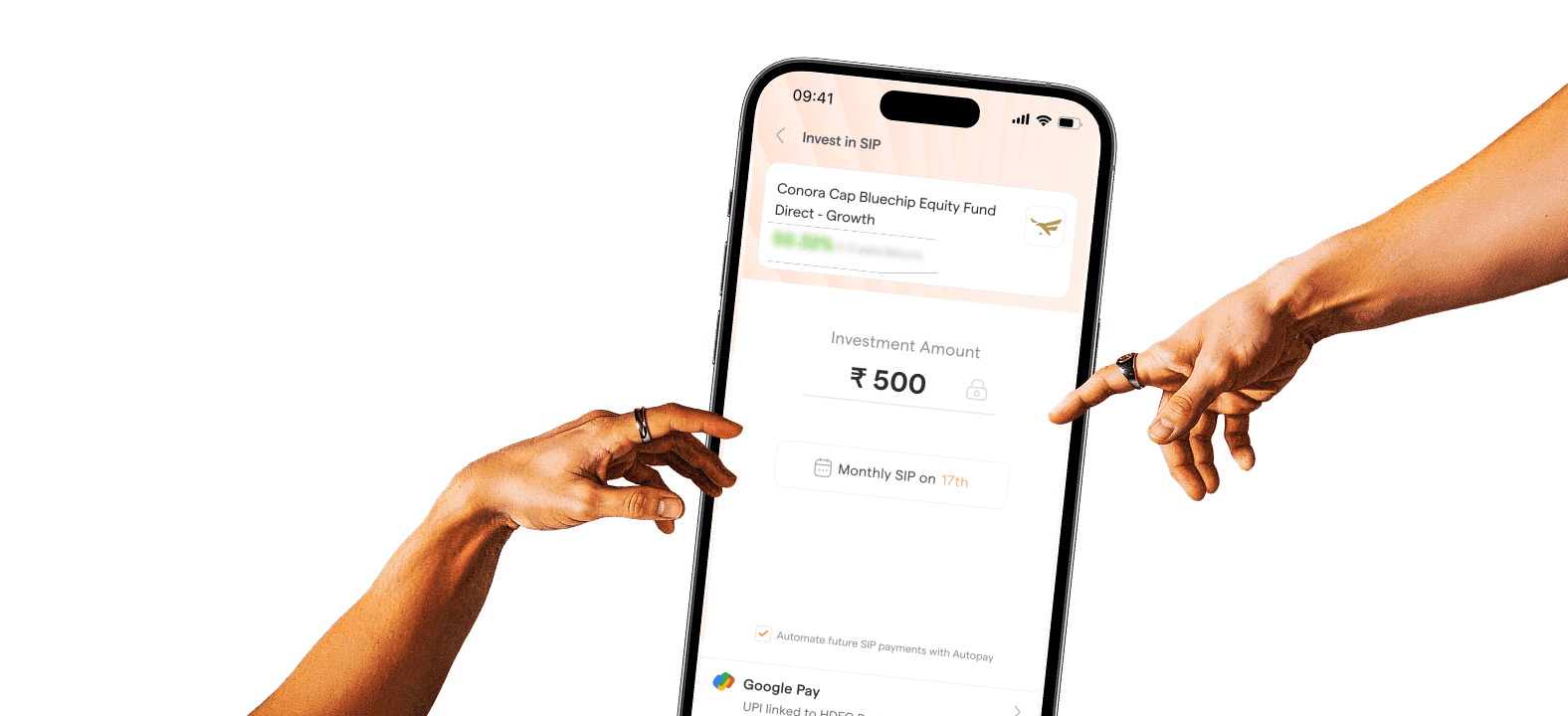

20% → Future you (Savings & investing)

This is where time really starts to work for you.

- SIPs in mutual funds

- Emergency fund

- Retirement contributions

This is the section that most people like to put off.

Since it does not have an immediate urgency.

But eventually,

This is the section which makes you financially independent.

Why it sounds easy but feels hard in real life

The structure is easy enough.

However, life is not structured.

A salary does not bring fixed behavioural patterns.

Expenses do not come in percentages.

Some months are difficult

Because of increased rent pressure.

Some months require travelling.

Other months may be full of unexpected expenses.

And all of a sudden,

The neat percentages begin to bend.

At that point, people realise: This principle does not apply to me.

The problem, however, is not the principle.

It lies in the expectation of absolute balance.

The real purpose most people miss

The 50 30 20 rule was not intended to become a strict money guideline.

It is only a visibility strategy.

It enables you to

Ask yourself three simple questions:

- Are my necessities taking up too much space?

- Is my living standard increasing faster than my earnings?

- Am I saving anything on a regular basis?

Generally,

Such questions are asked by people

When they think that their finances are low.

This philosophy helps them realise this much earlier.

Why people think it doesn’t work for them

Most people give it a try once and find that it doesn’t quite fit.

And that’s normal.

Because very few people start their financial lives

With a savings percentage of 20%.

The salary stages in the initial phase could be:

- High needs ratio

- Changing lifestyle patterns

- Inconsistencies in savings initially

That does not imply that the system is not working.

It only implies that the system is flexible in its nature,

Not rigid in design.

Even 5%-10% savings make an impact over time.

As financial skills are developed through experience, not perfection!

Where the rule actually works well

This rule works best when:

- Your income is consistent

- Expenses are more or less predictable

- Financial behaviour patterns are still being developed

That is why the 50 30 20 rule has been particularly appealing to young earners,

Why?

It provides a basic framework for making financial decisions

When everything is new.

Rather than asking yourself:

How much do I need to save?

You will already have a simple framework to work with.

It doesn’t make things easier.

It just makes them clearer.

Where it needs adjustment

It gets difficult to apply this rule where:

- Rent eats up a big chunk of money

- EMIs have already been earmarked

- Income varies every month

- Responsibilities are unequal

In such situations,

Trying to maintain percentages can lead to

Stress rather than clarity.

This is the reason why experienced people do not consider it fixed math.

They consider it a direction.

A more realistic version of the rule

In reality, it usually plays out like this:

- First, take care of the basics

- Then allow some room for lifestyle expenses

- Lastly, automate the rest into savings

It’s a bit more flexible.

But also realistic.

Since it caters to real-world situations rather than hypothetical ones.

So, does the 50-30-20 rule actually work?

Yes – but not as an absolute formula.

It serves as a decision filter.

It enables you to see the imbalance before it becomes ingrained.

As the reason for financial distress is rarely the absence of cash.

But rather the absence of clear financial structuring.

Which this rule subtly addresses.

Final Thoughts

50 30 20 rule is not a strategy for perfect budgeting.

It is a method of ensuring

That your money does not become unaccounted for.

You may find yourself unable to follow the exact percentages each month.

But if this approach helps you:

- Track how your money is being spent

- Save a bit more consistently

- Avoid complete financial chaos

Then, the 50-30-20 approach is working for you.

Because financial stability is never about perfection.

It’s created through simplicity…

Repeating enough times that it starts to count.